Backtrader 文档学习-Platform Concepts

Backtrader 文档学习-Platform Concepts

1.开始之前

导入backtrader ,以及backtrader 的指示器、数据反馈的模块 。

import backtrader as bt

import backtrader.indicators as btind

import backtrader.feeds as btfeeds

看看btind模块下有什么方法和属性:

obj_str = ''

for i in dir(btind):

if i[:1] != '_' :

obj_str += i + ','

print(obj_str)

指示器中的指标函数很多,方法属性如下:

ADX,ADXR,AO,APO,ATR,AbsPriceOsc,AbsolutePriceOscillator,AccDeOsc,AccelerationDecelerationOscillator,Accum,AdaptiveMovingAverage,AdaptiveMovingAverageEnvelope,AdaptiveMovingAverageOsc,AdaptiveMovingAverageOscillator,All,AllN,And,Any,AnyN,ApplyN,ArithmeticMean,AroonDown,AroonIndicator,AroonOsc,AroonOscillator,AroonUp,AroonUpDown,AroonUpDownOsc,AroonUpDownOscillator,Average,AverageDirectionalMovementIndex,AverageDirectionalMovementIndexRating,AverageTrueRange,AverageWeighted,AwesomeOsc,AwesomeOscillator,BBands,BaseApplyN,BollingerBands,BollingerBandsPct,CCI,Cmp,CmpEx,CointN,CommodityChannelIndex,CrossDown,CrossOver,CrossUp,CumSum,CumulativeSum,DEMA,DEMAEnvelope,DEMAOsc,DEMAOscillator,DI,DM,DMA,DMAEnvelope,DMAOsc,DMAOscillator,DMI,DPO,DV2,DemarkPivotPoint,DetrendedPriceOscillator,DicksonMA,DicksonMAEnvelope,DicksonMAOsc,DicksonMAOscillator,DicksonMovingAverage,DicksonMovingAverageEnvelope,DicksonMovingAverageOsc,DicksonMovingAverageOscillator,DirectionalIndicator,DirectionalMovement,DirectionalMovementIndex,DivByZero,DivZeroByZero,DoubleExponentialMovingAverage,DoubleExponentialMovingAverageEnvelope,DoubleExponentialMovingAverageOsc,DoubleExponentialMovingAverageOscillator,DownDay,DownDayBool,DownMove,EC,ECEnvelope,ECOsc,ECOscillator,EMA,EMAEnvelope,EMAOsc,EMAOscillator,Envelope,EnvelopeMixIn,ErrorCorrecting,ErrorCorrectingEnvelope,ErrorCorrectingOsc,ErrorCorrectingOscillator,ExpSmoothing,ExpSmoothingDynamic,ExponentialMovingAverage,ExponentialMovingAverageEnvelope,ExponentialMovingAverageOsc,ExponentialMovingAverageOscillator,ExponentialSmoothing,ExponentialSmoothingDynamic,FibonacciPivotPoint,FindFirstIndex,FindFirstIndexHighest,FindFirstIndexLowest,FindLastIndex,FindLastIndexHighest,FindLastIndexLowest,HMA,HMAEnvelope,HMAOsc,HMAOscillator,HeikinAshi,Highest,HullMA,HullMAEnvelope,HullMAOsc,HullMAOscillator,HullMovingAverage,HullMovingAverageEnvelope,HullMovingAverageOsc,HullMovingAverageOscillator,Hurst,HurstExponent,Ichimoku,If,Indicator,KAMA,KAMAEnvelope,KAMAOsc,KAMAOscillator,KST,KnowSureThing,LAGF,LRSI,LaguerreFilter,LaguerreRSI,LineActions,List,Logic,Lowest,MACD,MACDHisto,MACDHistogram,MAXINT,Max,MaxN,Mean,MeanDev,MeanDeviation,MetaMovAvBase,Min,MinN,MinusDI,MinusDirectionalIndicator,ModifiedMovingAverage,ModifiedMovingAverageEnvelope,ModifiedMovingAverageOsc,ModifiedMovingAverageOscillator,Momentum,MomentumOsc,MomentumOscillator,MovAv,MovingAverage,MovingAverageAdaptive,MovingAverageAdaptiveEnvelope,MovingAverageAdaptiveOsc,MovingAverageAdaptiveOscillator,MovingAverageBase,MovingAverageDoubleExponential,MovingAverageDoubleExponentialEnvelope,MovingAverageDoubleExponentialOsc,MovingAverageDoubleExponentialOscillator,MovingAverageExponential,MovingAverageExponentialEnvelope,MovingAverageExponentialOsc,MovingAverageExponentialOscillator,MovingAverageSimple,MovingAverageSimpleEnvelope,MovingAverageSimpleOsc,MovingAverageSimpleOscillator,MovingAverageSmoothed,MovingAverageSmoothedEnvelope,MovingAverageSmoothedOsc,MovingAverageSmoothedOscillator,MovingAverageTripleExponential,MovingAverageTripleExponentialEnvelope,MovingAverageTripleExponentialOsc,MovingAverageTripleExponentialOscillator,MovingAverageWeighted,MovingAverageWeightedEnvelope,MovingAverageWeightedOsc,MovingAverageWeightedOscillator,MovingAverageWilder,MovingAverageWilderEnvelope,MovingAverageWilderOsc,MovingAverageWilderOscillator,MultiLogic,MultiLogicReduce,NZD,NonZeroDifference,OLS_BetaN,OLS_Slope_InterceptN,OLS_TransformationN,OperationN,Or,Oscillator,OscillatorMixIn,PGO,PPO,PPOShort,PSAR,ParabolicSAR,PctChange,PctRank,PercPriceOsc,PercPriceOscShort,PercentChange,PercentRank,PercentagePriceOscillator,PercentagePriceOscillatorShort,PeriodN,PivotPoint,PlusDI,PlusDirectionalIndicator,PrettyGoodOsc,PrettyGoodOscillator,PriceOsc,PriceOscillator,RMI,ROC,ROC100,RSI,RSI_Cutler,RSI_EMA,RSI_SMA,RSI_SMMA,RSI_Safe,RSI_Wilder,RateOfChange,RateOfChange100,Reduce,ReduceN,RelativeMomentumIndex,RelativeStrengthIndex,SMA,SMAEnvelope,SMAOsc,SMAOscillator,SMMA,SMMAEnvelope,SMMAOsc,SMMAOscillator,SimpleMovingAverage,SimpleMovingAverageEnvelope,SimpleMovingAverageOsc,SimpleMovingAverageOscillator,SmoothedMovingAverage,SmoothedMovingAverageEnvelope,SmoothedMovingAverageOsc,SmoothedMovingAverageOscillator,StandardDeviation,StdDev,Stochastic,StochasticFast,StochasticFull,StochasticSlow,Sum,SumN,TEMA,TEMAEnvelope,TEMAOsc,TEMAOscillator,TR,TRIX,TSI,TripleExponentialMovingAverage,TripleExponentialMovingAverageEnvelope,TripleExponentialMovingAverageOsc,TripleExponentialMovingAverageOscillator,Trix,TrixSignal,TrueHigh,TrueLow,TrueRange,TrueStrengthIndicator,UltimateOscillator,UpDay,UpDayBool,UpMove,Vortex,WMA,WMAEnvelope,WMAOsc,WMAOscillator,WeightedAverage,WeightedMovingAverage,WeightedMovingAverageEnvelope,WeightedMovingAverageOsc,WeightedMovingAverageOscillator,WilderMA,WilderMAEnvelope,WilderMAOsc,WilderMAOscillator,WilliamsAD,WilliamsR,ZLEMA,ZLEMAEnvelope,ZLEMAOsc,ZLEMAOscillator,ZLInd,ZLIndEnvelope,ZLIndOsc,ZLIndOscillator,ZLIndicator,ZLIndicatorEnvelope,ZLIndicatorOsc,ZLIndicatorOscillator,ZeroLagEma,ZeroLagEmaEnvelope,ZeroLagEmaOsc,ZeroLagEmaOscillator,ZeroLagExponentialMovingAverage,ZeroLagExponentialMovingAverageEnvelope,ZeroLagExponentialMovingAverageOsc,ZeroLagExponentialMovingAverageOscillator,ZeroLagIndicator,ZeroLagIndicatorEnvelope,ZeroLagIndicatorOsc,ZeroLagIndicatorOscillator,absolute_import,accdecoscillator,alias,aroon,atr,awesomeoscillator,basicops,bollinger,bt,cci,cmp,contrib,crossover,dema,deviation,directionalmove,division,dma,dpo,dv2,ema,envelope,functools,haD,haDelta,hadelta,heikinashi,hma,hurst,ichimoku,kama,kst,linename,lrsi,mabase,macd,map,math,module,momentum,movav,movname,newaliases,newcls,newclsdct,newclsdoc,newclsname,ols,operator,oscillator,percentchange,percentrank,pivotpoint,prettygoodoscillator,priceoscillator,print_function,psar,range,rmi,rsi,sma,smma,stochastic,suffix,sys,trix,tsi,ultimateoscillator,unicode_literals,williams,with_metaclass,wma,zlema,zlind,

也可以直接通过bt导入下面的模块feeds indicators

import backtrader as bt

thefeed = bt.feeds.OneOfTheFeeds(...)

theind = bt.indicators.SimpleMovingAverage(...)

2.数据读入-无处不在

所有的策略都基于数据,平台端用户不用考虑如何接收数据。

Data Feeds are automagically provided member variables to the strategy in the form of an array and shortcuts to the array positions

数据源是以数组的形式或者对数组位置快捷访问的方式提供给strategy(策略)作为成员变量使用的。

这句话需要好好理解。

数组的形式: self.datas[0].close

数组位置快捷访问:self.data0.close

class MyStrategy(bt.Strategy):

params = dict(period=20)

def __init__(self):

sma = btind.SimpleMovingAverage(self.datas[0], period=self.params.period)

print(sma)

# Keep a reference to the "close" line in the data[0] dataseries

self.dataclose = self.datas[0].close

self.dataclosetest = self.data0.close

print('-'* 20,'close','-' * 20 )

print(self.dataclose[0])

print(self.dataclosetest[0])

执行结果

sma 的数据类型backtrader.indicators.sma.SimpleMovingAverage

<backtrader.indicators.sma.SimpleMovingAverage object at 0x7f616bd7c820>

-------------------- close --------------------

133.01

133.01

Data Feeds get added to the platform and they will show up inside the strategy in the sequential order in which they were added to the system.

SQL语句按日期排序,不论是正序还是逆序desc ,到BackTrader中,都是按时间倒序排列,[0]是最后的日期。

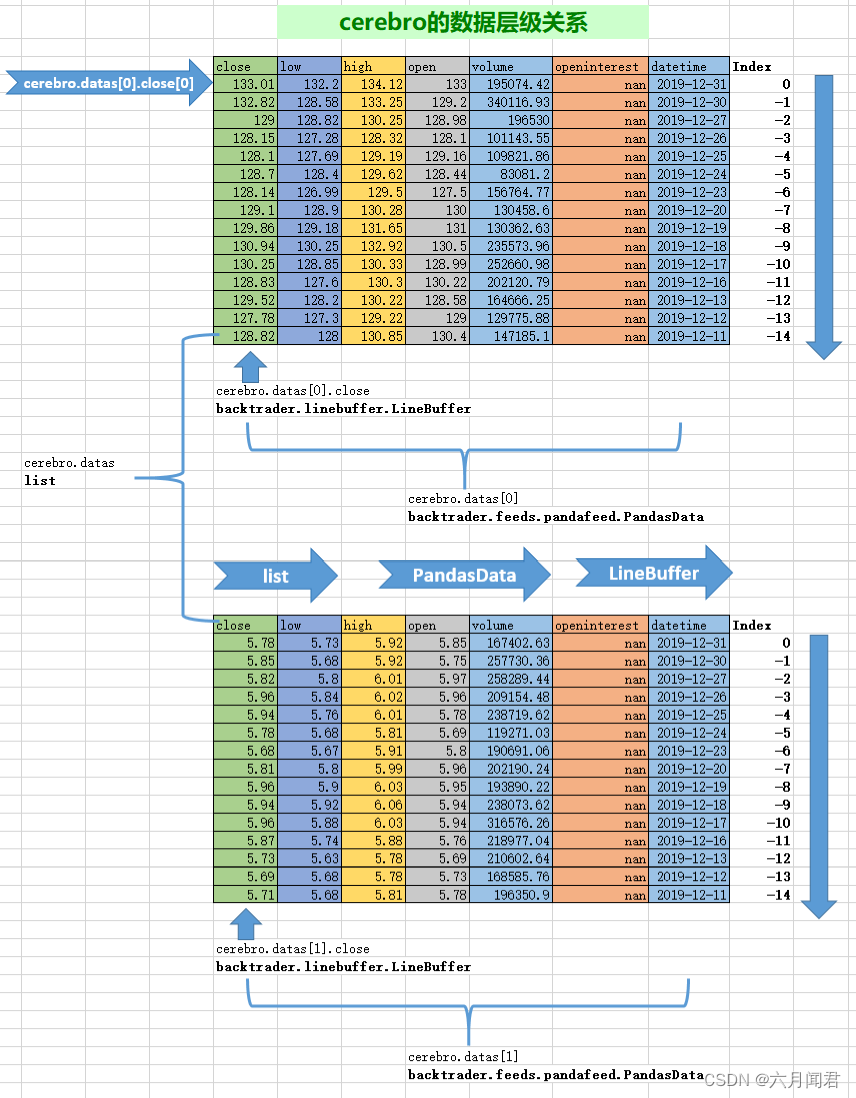

3.快捷访问数据

self.datas数组项可以通过自动成员变量直接访问:

self.data targets self.datas[0]

self.dataX targets self.datas[X]

下面好好测试一下BackTrader的数据访问,数据之间的关系。

#<class 'backtrader.linebuffer.LineBuffer'>

print(type(cerebro.datas[0].close))

#<class 'backtrader.feeds.pandafeed.PandasData'>

print(type(cerebro.datas[0]))

#<class 'list'>

print(type(cerebro.datas))

# ('close', 'low', 'high', 'open', 'volume', 'openinterest', 'datetime')

print(cerebro.datas[0].getlinealiases())

结果如下:

<class 'backtrader.linebuffer.LineBuffer'>

<class 'backtrader.feeds.pandafeed.PandasData'>

<class 'list'>

('close', 'low', 'high', 'open', 'volume', 'openinterest', 'datetime')

说明:

- 1、cerebro.datas数据集的类型是 <class ‘list’> ,对应载入cerebro的股票数据,可以是多个股票,就是股票的集合。

- 2、cerebro.datas[0]是<class ‘backtrader.feeds.pandafeed.PandasData’>,其实与dataframe类似,包括以下列:(‘close’, ‘low’, ‘high’, ‘open’, ‘volume’, ‘openinterest’, ‘datetime’)的集合。

-3、cerebro.datas[0].close就是dataframe的一列数据,BackTrader称之为Line <class ‘backtrader.linebuffer.LineBuffer’> 。 - 4、cerebro.datas[0].close[0] 就是访问到数据的元素,实际数据值。

- 5、cerebro.datas[0]都是按时间顺序逆序的,第一个元素index是0 ,下一个是-1 ,以此类推。

- 6、时间序列必须用内置方法处理

print(cerebro.datas[0].datetime[0])

print(pd.to_datetime(cerebro.datas[0].datetime[0],unit='s'))

print(bt.num2date(cerebro.datas[0].datetime[0]))

结果如下:

737424.0

1970-01-09 12:50:24

2019-12-31 00:00:00

直接访问datetime列 ,是浮点数。

开始用pd.to_datetime 函数,转换的时间是1970年,迷惑很长时间。

重要:必须用自带的函数转换时间 bt.num2date()!!!

4.默认数据载入

class MyStrategy(bt.Strategy):

params = dict(period=20)

def __init__(self):

sma = btind.SimpleMovingAverage(period=self.params.period)

...

self.data has been completely removed from the invocation of SimpleMovingAverage. If this is done, the indicator (in this case the SimpleMovingAverage) receives the first data of the object in which is being created (the Strategy), which is self.data (aka self.data0 or self.datas[0])

默认使用的self是什么?

如果只有一个数据源,cerebro只载入一个股票数据,不用显式指定,系统会缺省使用self.datas[0],self.data=self.data0=self.datas[0] ,也就是第一个加入的数据源 。所以说self.data 就没有显式出现在调用SMA指示器 。

如果有多个载入数据,还是注明好,清晰可读。

5. 一切都是数据载入

class MyStrategy(bt.Strategy):

#定义策略全局参数

params = dict(period1=20, period2=25, period3=10, period4)

def __init__(self):

# 使用SMA指示器载入datas[0],使用参数1

sma1 = btind.SimpleMovingAverage(self.datas[0], period=self.p.period1)

# This 2nd Moving Average operates using sma1 as "data"

# 使用第一个SMA指示器数据再次作为SMA的数据载入,使用参数2

sma2 = btind.SimpleMovingAverage(sma1, period=self.p.period2)

# New data created via arithmetic operation

# 随意的计算

something = sma2 - sma1 + self.data.close

# This 3rd Moving Average operates using something as "data"

# 随意计算的结果作为第三次SMA数据载入,使用参数3

sma3 = btind.SimpleMovingAverage(something, period=self.p.period3)

# Comparison operators work too ...

# 比较后取大值 ,有点疑问 ?

greater = sma3 > sma1

# Pointless Moving Average of True/False values but valid

# This 4th Moving Average operates using greater as "data"

# 比较后结果第四次载入SMA指示器,使用参数4

sma3 = btind.SimpleMovingAverage(greater, period=self.p.period4)

...

总而言之,所有的数据转换变化后,都可以作为数据载入,再次进行运算。

6. 参数

在backtrader中,所有的类都按照如下方法来使用参数:

1、声明一个带有缺省值的参数作为类的一个属性(元组或者字典结构)。

2、关键字类型参数(kwargs)会扫描匹配的参数,将值赋值给对应的参数,完成后从kwargs删除。

3、这些参数都可以在类实例中通过访问成员变量self.params(可以简写为self.p)来使用。

使用元组 tuple

class MyStrategy(bt.Strategy):

params = (('period', 20),)

def __init__(self):

sma = btind.SimpleMovingAverage(self.data, period=self.p.period)

使用字典dict

class MyStrategy(bt.Strategy):

params = dict(period=20)

def __init__(self):

sma = btind.SimpleMovingAverage(self.data, period=self.p.period)

7.Lines 关键的概念

从使用用户(通常是strategy)的角度来说,就是包括一个或多个line,这些line是一系列的数据,在图中可以形成一条线(line)。line是数组,不是pd.series ,没有index 。

class MyStrategy(bt.Strategy):

params = dict(period=20)

def __init__(self):

self.movav = btind.SimpleMovingAverage(self.data, period=self.p.period)

def next(self):

if self.movav.lines.sma[0] > self.data.lines.close[0]:

print(round(self.movav.lines.sma[0],2),self.data.lines.close[0],'Simple Moving Average is greater than the closing price')

执行结果:

83.34 74.4 Simple Moving Average is greater than the closing price

83.16 75.1 Simple Moving Average is greater than the closing price

83.01 76.6 Simple Moving Average is greater than the closing price

82.92 80.1 Simple Moving Average is greater than the closing price

82.82 79.64 Simple Moving Average is greater than the closing price

82.69 78.52 Simple Moving Average is greater than the closing price

82.36 76.1 Simple Moving Average is greater than the closing price

81.87 74.28 Simple Moving Average is greater than the closing price

... ...

self.movav:这个是一个SimpleMovingAverage的指标(indicator),本身就包含一个具有lines属性的sma。这里特殊注意一下,计算SimpleMovingAverage使用的self.data,没有指定具体Line的话,缺省用的是close价进行计算。

简单的方法访问lines:

xxx.lines 可以简化为 xxx.l

xxx.lines.name可以简化为xxx.lines_name

一些复杂的对象也可以通过如下方法访问:

self.data_name 等于 self.data.lines.name

如果有多个变量的话,也可以self.data1_name 替代self.data1.lines.name

此外,Line的名字也可以通过如下方式访问:

self.data.close and self.movav.sma

class MyStrategy(bt.Strategy):

params = dict(period=20)

def __init__(self):

self.movav = btind.SimpleMovingAverage(self.data, period=self.p.period)

def next(self):

# 数据集0 收盘价在110和120

if (self.datas[0].close[0] > 110.0) & (self.datas[0].close[0] < 120.0):

print(bt.num2date(self.datas[0].datetime[0]),'self.datas[0].close[0] > 110.0')

# 数据集1 收盘价在110和120

if self.datas[1].close[0] > 9.0:

print(bt.num2date(self.datas[1].datetime[0]),'self.datas[1].close[0] > 9.0')

# 数据集SMA 收盘价在88和90

if (self.movav.lines.sma[0] > 88) & (self.movav.sma[0] < 90) :

print(round(self.movav.lines.sma[0],2),'self.movav.lines.sma[0] > 88')

print(self.movav.getlinealiases())

#print(cerebro.datas[0].getlinealiases())

结果如下:

2018-04-18 00:00:00 self.datas[1].close[0] > 9.0

2018-04-24 00:00:00 self.datas[1].close[0] > 9.0

2018-04-25 00:00:00 self.datas[1].close[0] > 9.0

2018-04-26 00:00:00 self.datas[1].close[0] > 9.0

2019-04-09 00:00:00 self.datas[0].close[0] > 110.0

88.78 self.movav.lines.sma[0] > 88

('sma',)

89.64 self.movav.lines.sma[0] > 88

('sma',)

2019-06-20 00:00:00 self.datas[0].close[0] > 110.0

2019-06-21 00:00:00 self.datas[0].close[0] > 110.0

2019-06-24 00:00:00 self.datas[0].close[0] > 110.0

2019-06-25 00:00:00 self.datas[0].close[0] > 110.0

2019-06-26 00:00:00 self.datas[0].close[0] > 110.0

2019-06-27 00:00:00 self.datas[0].close[0] > 110.0

2019-06-28 00:00:00 self.datas[0].close[0] > 110.0

2019-07-24 00:00:00 self.datas[0].close[0] > 110.0

2019-08-01 00:00:00 self.datas[0].close[0] > 110.0

2019-08-02 00:00:00 self.datas[0].close[0] > 110.0

2019-08-05 00:00:00 self.datas[0].close[0] > 110.0

2019-08-07 00:00:00 self.datas[0].close[0] > 110.0

2019-08-09 00:00:00 self.datas[0].close[0] > 110.0

需要好好说明一下:

- 简写示例

if (self.movav.lines.sma[0] > 88) & (self.movav.sma[0] < 90) :

- 多数据源

两种方式引用

self.movav.lines.sma[0] = self.movav.sma[0]

cerebro载入两个股票数据。

特别注意:调用datas ,有s

self.datas[0].close[0]

self.datas[0].close[0]

self.datas[0].close[0]

- SMA指示器调用后,是数组,没有日期字段!!!

开始也想增加打印日期,

print(bt.num2date(self.movav.datetime[0]) 无日期

只有一列

print(self.movav.getlinealiases())

('sma',)

未完待续!!!

本文来自互联网用户投稿,该文观点仅代表作者本人,不代表本站立场。本站仅提供信息存储空间服务,不拥有所有权,不承担相关法律责任。 如若内容造成侵权/违法违规/事实不符,请联系我的编程经验分享网邮箱:veading@qq.com进行投诉反馈,一经查实,立即删除!