机器学习——线性模型(二)

【说明】文章内容来自《机器学习——基于sklearn》,用于学习记录。若有争议联系删除。

1、优化方法

线性回归最小二乘法的两种求解方法(即优化方法)分别是正规方程和梯度下降。

1.1?正规方程

????????最小二乘法可以将误差方程转化为有确定解的代数方程组(其方程式数目正好等于未知数的个数),从而可求解出这些未知数。这个有确定解的代数方程组称为最小二乘法估计的正规方程(normal equation)。

????????正规方程法也称为解析法,采用 Sklearn提供的LinearRegression函数实现。

1.2 正规方法对波士顿房价预测

from sklearn.model_selection import train_test_split

from sklearn.preprocessing import StandardScaler

from sklearn.linear_model import LinearRegression

from sklearn.metrics import mean_squared_error

import pandas as pd

import numpy as np

data_url = "http://lib.stat.cmu.edu/datasets/boston"

raw_df = pd.read_csv(data_url, sep="\s+", skiprows=22, header=None)

data = np.hstack([raw_df.values[::2, :], raw_df.values[1::2, :2]])

target = raw_df.values[1::2, 2]

def linear1():

x_train, x_test, y_train, y_test = train_test_split(data, target, random_state = 33, test_size = 0.25)

transfer = StandardScaler()

x_train = transfer.fit_transform(x_train)

x_test = transfer.transform(x_test)

lr = LinearRegression()

lr.fit(x_train, y_train)

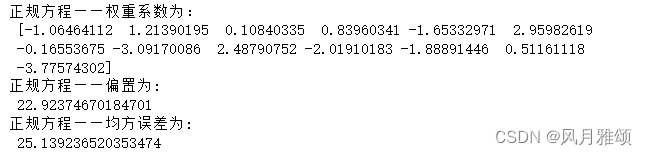

print('正规方程——权重系数为:\n', lr.coef_)

print('正规方程——偏置为:\n', lr.intercept_)

y_predict = lr.predict(x_test)

error = mean_squared_error(y_test, y_predict)

print('正规方程——均方误差为:\n', error)

return None

if __name__ == '__main__':

linear1()【运行结果】

1.3?梯度下降

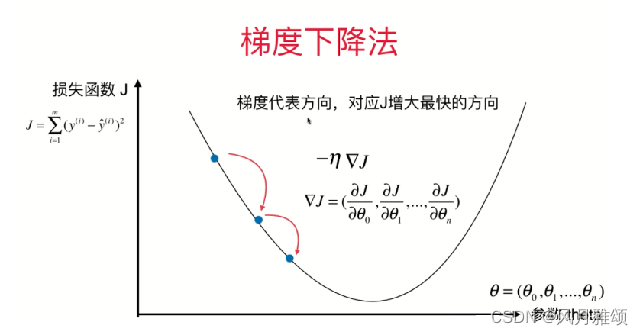

????????梯度下降(gradient descent)主要用于多元线性回归算法,通过迭代找到目标函数的最小值,或者收敛到最小值。梯度下降法的思想可以类比为下山的过程。当一个人从山顶需要以最快速度下山时,每一刻都以当前所处的位置为基准,寻找从这个位置出发坡度最陡的方向下降。梯度下降法的原理如图所示。

Sklearn提供了SGDRegressor 方法用于梯度下降,格式如下:

SGDRegressor(loss='squared_loss', fit_intercept= True, learning_rate='invscaling')【参数说明】

- loss= 'squared _loss':损失函数是最小二乘法。

- fit_intercept:是否计算截距,默认为True.

- learning_rate= 'invscaling':指定学习率,即下降的步长。

1.4 用梯度下降法对美国波士顿地区房价进行预测。

from sklearn.model_selection import train_test_split

from sklearn.preprocessing import StandardScaler

from sklearn.linear_model import SGDRegressor

from sklearn.metrics import mean_squared_error

import pandas as pd

import numpy as np

data_url = "http://lib.stat.cmu.edu/datasets/boston"

raw_df = pd.read_csv(data_url, sep="\s+", skiprows=22, header=None)

data = np.hstack([raw_df.values[::2, :], raw_df.values[1::2, :2]])

target = raw_df.values[1::2, 2]

def linear2():

x_train, x_test, y_train, y_test = train_test_split(data, target, random_state = 33, test_size = 0.25)

transfer = StandardScaler()

x_train = transfer.fit_transform(x_train)

x_test = transfer.transform(x_test)

sgdr = SGDRegressor()

sgdr.fit(x_train, y_train)

print('梯度下降——权重系数为:\n', sgdr.coef_)

print('梯度下降——偏置为:\n', sgdr.intercept_)

y_predict = sgdr.predict(x_test)

error = mean_squared_error(y_test, y_predict)

print('正规方程——均方误差为:\n', error)

return None

if __name__ == '__main__':

linear2()【运行结果】

2、岭回归

2.1 简介

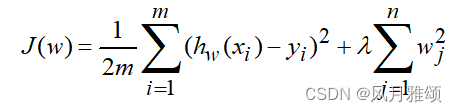

????????岭回归又称为L2正则化。该方法保留全部特征变量,只降低特征变量的系数值,通过弱化参数之间的差异性来避免过拟合。其数学表达式如下:

????????岭回归通过对回归系数施加惩罚来解决过拟合问题。具体来说,通过在最小二乘法项后增加L2范数(惩罚项系数)来控制线性模型的复杂程度,从而使模型更加稳健。另一种正则化称为L1正则化,又称为Lasso回归,它通过让参数向量中的许多特征趋近0使它们失去对优化目标的贡献,从此实现目标最小化。

Sklearn 提供了Ridge函数来实现岭回归,格式如下:

sklearn.linear_model.Ridge (alpha=1.0, fit_intercept=True, solver='auto',normalize=False)【参数说明】

- alpha:正则化力度,即惩罚项系数。

- fit_intercept:是否增加偏置。

- solver:优化器

- normalize:是否进行数据标准化。

属性如下:

- coef_:数组类型,用于权重向量。

- intercept_:截距。当fit _intercept=False时,该属性值为0.0。

方法如下:

- fit(X,y):训练模型。

- get_params():获取此估计器的参数。

- predict(X):使用线性模型进行预测,返回预测值。

- score(X,y):返回预测性能的得分。

- set_params():设置此估计器的参数。

2.2 岭回归示例

import numpy as np

import matplotlib.pyplot as plt

from sklearn import linear_model

data=[[83.0, 234.289, 235.6, 159.0, 107.608, 1947., 60.323],

[88.5, 259.426, 232.5, 145.6, 108.632, 1948., 61.122],

[88.2, 258.054, 368.2, 161.6, 109.773, 1949., 60.171],

[89.5, 284.599, 335.1, 165.0, 110.929, 1950., 61.187],

[96.2, 328.975, 209.9, 309.9, 112.075, 1951., 63.221],

[98.1, 346.999, 193.2, 359.4, 113.27, 1952., 63.639],

[99.0, 365.385, 187., 354.7, 115.094, 1953., 64.989],

[100.0, 363.112, 357.8, 335.0, 116.219, 1954., 63.761],

[101.2, 397.469, 290.4, 304.8, 117.388, 1955., 66.019],

[104.6, 419.18, 282.2, 285.7, 118.734, 1956., 67.857],

[108.4, 442.769, 293.6, 279.8, 120.445, 1957., 68.169],

[110.8, 444.546, 468.1, 263.7, 121.95, 1958., 66.513],

[112.6, 482.704, 381.3, 255.2, 123.366, 1959., 68.655],

[114.2, 502.601, 393.1, 251.4, 125.368, 1960., 69.564],

[115.7, 518.173, 480.6, 257.2, 127.852, 1961., 69.331],

[116.9, 554.894, 400.7, 282.7, 130.081, 1962., 70.5511]]

data = np.array(data)

X_data = data[:,1:]

y_data = data[:,0]

print(X_data)

print(y_data)

#岭回归模型

alpha = 0.5

model = linear_model.Ridge(alpha)

model.fit(X_data, y_data)

#返回模型的估计系数

print(model.coef_)

#评分

model.score(X_data,y_data)

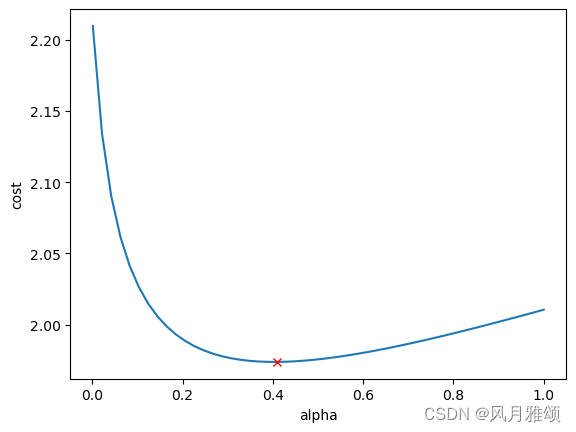

#创建模型,开始训练,生成50个alpha系数

alphas=np.linspace(0.001, 1, 50)

#RidgeCV表示岭回归交叉检验,类似于留一交叉验证法

#它在训练时保留一个样本,用这个样本进行测试

cv_model = linear_model.RidgeCV(alphas, store_cv_values = True)

cv_model.fit(X_data, y_data)

#最佳的alpha

best_alpha = cv_model.alpha_

print(best_alpha)

#交叉验证的结果

print(cv_model.cv_values_)

print(cv_model.cv_values_.shape)

#结果中(16,50)指数据被拆分为16份,做了16次训练和测试,每次训练集使用15份数据

#测试集使用1份数据,每次使用50个alpha值进行训练

#针对所有alpha值计算出的损失值

plt.plot(alphas, cv_model.cv_values_.mean(axis=0))

#最佳点

min_cost=min(cv_model.cv_values_.mean(axis=0))

plt.plot(best_alpha, min_cost, 'rx')

plt.xlabel('alpha')

plt.ylabel('cost')

plt.show()【运行结果】

2.3 alpha参数

????????岭回归的alpha参数作为惩罚项的系数,对应于其他线性模型(如逻辑回归LinearSVC)中的C参数。下面通过调整alpha参数值分析线性模型的拟合程度。

from sklearn.model_selection import train_test_split

from sklearn.datasets import load_diabetes

x, y = load_diabetes().data, load_diabetes().target

x_train, x_test, y_train, y_test = train_test_split(x, y, random_state = 8)

from sklearn.linear_model import Ridge

ridge01 = Ridge(alpha = 0.1).fit(x_train, y_train)

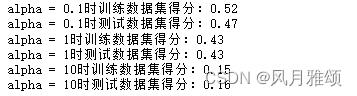

print('alpha = 0.1时训练数据集得分:{:.2f}'.format(ridge01.score(x_train, y_train)))

print('alpha = 0.1时测试数据集得分:{:.2f}'.format(ridge01.score(x_test, y_test)))

ridge1 = Ridge(alpha = 1).fit(x_train, y_train)

print('alpha = 1时训练数据集得分:{:.2f}'.format(ridge1.score(x_train, y_train)))

print('alpha = 1时测试数据集得分:{:.2f}'.format(ridge1.score(x_test, y_test)))

ridge10 = Ridge(alpha = 10).fit(x_train, y_train)

print('alpha = 10时训练数据集得分:{:.2f}'.format(ridge10.score(x_train, y_train)))

print('alpha = 10时测试数据集得分:{:.2f}'.format(ridge10.score(x_test, y_test)))【运行结果】

3、案例

3.1 线性回归和岭回归用于糖尿病预测

#线性回归

from sklearn.model_selection import train_test_split

from sklearn.linear_model import LinearRegression

from sklearn.datasets import load_diabetes

x, y = load_diabetes().data, load_diabetes().target

x_train, x_test, y_train, y_test = train_test_split(x, y, random_state = 8)

lr = LinearRegression().fit(x_train, y_train)

print('训练数据集得分:{:.2f}'.format(lr.score(x_train, y_train)))

print('测试数据集得分:{:.2f}'.format(lr.score(x_test, y_test)))

#岭回归

from sklearn.model_selection import train_test_split

from sklearn.linear_model import Ridge

from sklearn.datasets import load_diabetes

x, y = load_diabetes().data, load_diabetes().target

x_train, x_test, y_train, y_test = train_test_split(x, y, random_state = 8)

ridge = Ridge().fit(x_train, y_train)

print('训练数据集得分:{:.2f}'.format(ridge.score(x_train, y_train)))

print('测试数据集得分:{:.2f}'.format(ridge.score(x_test, y_test)))3.2 最小二乘法和岭回归用于波士顿房价预测

#最小二乘法和领回归应用波士顿

from sklearn import datasets

import numpy as np

import matplotlib.pyplot as plt

import pandas as pd

data_url = "http://lib.stat.cmu.edu/datasets/boston"

raw_df = pd.read_csv(data_url, sep="\s+", skiprows=22, header=None)

data = np.hstack([raw_df.values[::2, :], raw_df.values[1::2, :2]])

target = raw_df.values[1::2, 2]

x = data

y = target

sampleRatio=0.5 #划分训练集和测试集,各用一半数据

m=len(x)

sampleBoundary=int(m* sampleRatio)

myshuffle=list(range(m)) #range返回序列

np.random.shuffle(myshuffle) # shuffle将序列内的元素全部随机排序

#分别取出训练集和测试集的数据

train_fea=x[myshuffle[sampleBoundary:]]#前一半数据作为训练集

train_tar=y[myshuffle[sampleBoundary:]]

test_fea=x[myshuffle[:sampleBoundary]]#后一半数据作为测试集

test_tar=y[myshuffle[:sampleBoundary]]

#使用最小二乘线性回归进行拟合

from sklearn import linear_model

#最小二乘线性

lr=linear_model.LinearRegression()

#拟合

lr.fit(train_fea, train_tar)

#得到预测值集合

y=lr.predict(test_fea)

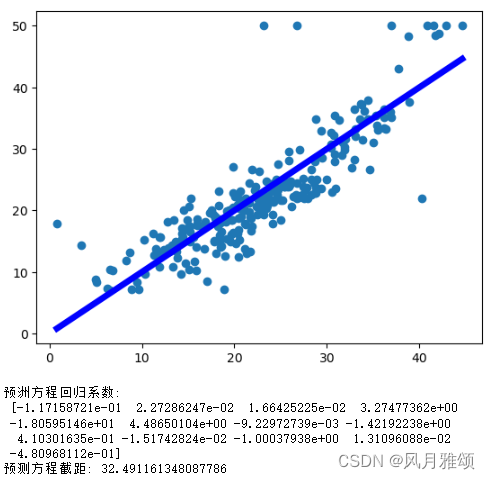

plt.scatter(y,test_tar) #画出散点图,横轴是预测值,纵轴是真实值

#将实际房价数据与预测数据对比,接近中间直钱的数据表示预测准确

plt.plot([y.min(),y.max()],[y.min(),y.max()],'b',lw = 5)

#直线的起点为(y,min(),y.min()),终点是(y.max(),y.max())

plt.show()

coef=lr.coef_

intercept = lr.intercept_

print("预洲方程回归系数:\n",coef)

print("预测方程截距:",intercept)【运行结果】

import numpy as np

import matplotlib.pyplot as plt

import pandas as pd

from sklearn.model_selection import train_test_split

from sklearn.preprocessing import StandardScaler

from sklearn.linear_model import Ridge

from sklearn.metrics import mean_squared_error

data_url = "http://lib.stat.cmu.edu/datasets/boston"

raw_df = pd.read_csv(data_url, sep="\s+", skiprows=22, header=None)

data = np.hstack([raw_df.values[::2, :], raw_df.values[1::2, :2]])

target = raw_df.values[1::2, 2]

def linear3():

x_train, x_test, y_train, y_test = train_test_split(data, target, random_state = 33, test_size = 0.25)

transfer = StandardScaler()

#分别对训练和测试数据的特征以及目标值进行标准化处理

x_train = transfer.fit_transform(x_train)

x_test = transfer.transform(x_test)

#预估器选择岭回归

estimator = Ridge()

estimator.fit(x_train, y_train)

#得出模型,输出回归系数和偏置

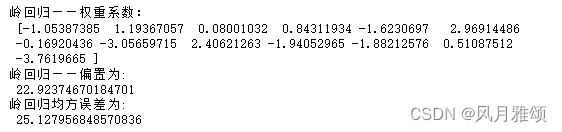

print('岭回归——权重系数:\n',estimator.coef_)

print('岭回归——偏置为:\n',estimator.intercept_)

y_predict = estimator.predict(x_test)

error = mean_squared_error(y_test, y_predict)

print('岭回归均方误差为:\n',error)

return None

if __name__ == '__main__':

linear3()【运行结果】

3.3 逻辑回归应用于鸢尾花分类

from sklearn.decomposition import PCA

from sklearn.datasets import load_iris

from sklearn.linear_model import LogisticRegression

import matplotlib.pyplot as plt

import numpy as np

plt.rcParams['font.sans-serif'] = ['SimHei']

plt.rcParams['font.family'] = 'sans-serif'

plt.rcParams['axes.unicode_minus'] = False

iris = load_iris()

iris_data = iris.data

iris_target = iris.target

print(iris_data.shape)

pca = PCA(n_components = 2)#特征降维

x = pca.fit_transform(iris_data)

print(x.shape)

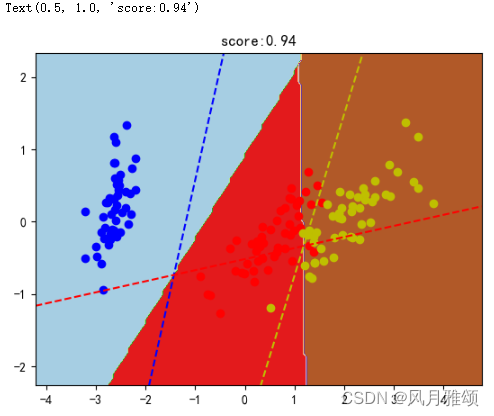

f = plt.figure()

ax = f.add_subplot(111)

ax.plot(x[:,0][iris_target == 0],x[:, 1][iris_target == 0], 'bo')

ax.scatter(x[:,0][iris_target == 1], x[:, 1][iris_target == 1], c = 'r')

ax.scatter(x[:, 0][iris_target == 2], x[:, 1][iris_target == 2], c = 'y')

ax.set_title('数据分布图')

plt.show ()

clf=LogisticRegression(multi_class = 'ovr', solver = 'lbfgs', class_weight={0:1, 1:1, 2:1})

clf.fit(x, iris_target)

score = clf.score (x, iris_target)

x0min, x0max = x[:, 0].min(), x[:, 0].max()

x1min, x1max = x[:, 1].min(), x[:, 1].max ()

h=0.05

xx, yy = np.meshgrid(np.arange (x0min - 1, x0max + 1, h), np.arange(x1min -1, x1max+1, h))

x_ = xx.reshape([xx.shape[0] * xx.shape[1], 1])

y_ = yy.reshape([yy.shape[0] * yy.shape[1], 1])

test_x = np.c_[x_, y_]

test_predict = clf.predict(test_x)

z = test_predict.reshape (xx.shape)

plt.contourf(xx, yy, z, cmap = plt.cm.Paired)

plt.axis('tight')

colors = 'bry'

for i, color in zip(clf.classes_, colors):

idx = np.where(iris_target == i)

plt.scatter(x[idx, 0], x[idx, 1], c = color, cmap = plt.cm.Paired)

xmin,xmax = plt.xlim()

coef = clf.coef_

intercept = clf.intercept_

def line(c, x0):

return (-coef[c,0]*x0 - intercept[c]) /coef[c, 1]

for i, color in zip(clf.classes_, colors):

plt.plot([xmin, xmax], [line(i, xmin), line(i, xmax)], color = color, linestyle ='--')

plt.title("score:{0}".format(score))【运行结果】

? ? ? ??

? ? ? ??

本文来自互联网用户投稿,该文观点仅代表作者本人,不代表本站立场。本站仅提供信息存储空间服务,不拥有所有权,不承担相关法律责任。 如若内容造成侵权/违法违规/事实不符,请联系我的编程经验分享网邮箱:veading@qq.com进行投诉反馈,一经查实,立即删除!